Trendline Breaks with Multi Fibonacci Supertrend StrategyTMFS Strategy: Advanced Trendline Breakouts with Multi-Fibonacci Supertrend

Elevate your algorithmic trading with institutional-grade signal confluence

Strategy Genesis & Evolution

This advanced trading system represents the culmination of a personal research journey, evolving from my custom " Multi Fibonacci Supertrend with Signals " indicator into a comprehensive trading strategy. Built upon the exceptional trendline detection methodology pioneered by LuxAlgo in their " Trendlines with Breaks " indicator, I've engineered a systematic framework that integrates multiple technical factors into a cohesive trading system.

Core Fibonacci Principles

At the heart of this strategy lies the Fibonacci sequence application to volatility measurement:

// Fibonacci-based factors for multiple Supertrend calculations

factor1 = input.float(0.618, 'Factor 1 (Weak/Fibonacci)', minval = 0.01, step = 0.01)

factor2 = input.float(1.618, 'Factor 2 (Medium/Golden Ratio)', minval = 0.01, step = 0.01)

factor3 = input.float(2.618, 'Factor 3 (Strong/Extended Fib)', minval = 0.01, step = 0.01)

These precise Fibonacci ratios create a dynamic volatility envelope that adapts to changing market conditions while maintaining mathematical harmony with natural price movements.

Dynamic Trendline Detection

The strategy incorporates LuxAlgo's pioneering approach to trendline detection:

// Pivotal swing detection (inspired by LuxAlgo)

pivot_high = ta.pivothigh(swing_length, swing_length)

pivot_low = ta.pivotlow(swing_length, swing_length)

// Dynamic slope calculation using ATR

slope = atr_value / swing_length * atr_multiplier

// Update trendlines based on pivot detection

if bool(pivot_high)

upper_slope := slope

upper_trendline := pivot_high

else

upper_trendline := nz(upper_trendline) - nz(upper_slope)

This adaptive trendline approach automatically identifies key structural market boundaries, adjusting in real-time to evolving chart patterns.

Breakout State Management

The strategy implements sophisticated state tracking for breakout detection:

// Track breakouts with state variables

var int upper_breakout_state = 0

var int lower_breakout_state = 0

// Update breakout state when price crosses trendlines

upper_breakout_state := bool(pivot_high) ? 0 : close > upper_trendline ? 1 : upper_breakout_state

lower_breakout_state := bool(pivot_low) ? 0 : close < lower_trendline ? 1 : lower_breakout_state

// Detect new breakouts (state transitions)

bool new_upper_breakout = upper_breakout_state > upper_breakout_state

bool new_lower_breakout = lower_breakout_state > lower_breakout_state

This state-based approach enables precise identification of the exact moment when price breaks through a significant trendline.

Multi-Factor Signal Confluence

Entry signals require confirmation from multiple technical factors:

// Define entry conditions with multi-factor confluence

long_entry_condition = enable_long_positions and

upper_breakout_state > upper_breakout_state and // New trendline breakout

di_plus > di_minus and // Bullish DMI confirmation

close > smoothed_trend // Price above Supertrend envelope

// Execute trades only with full confirmation

if long_entry_condition

strategy.entry('L', strategy.long, comment = "LONG")

This strict requirement for confluence significantly reduces false signals and improves the quality of trade entries.

Advanced Risk Management

The strategy includes sophisticated risk controls with multiple methodologies:

// Calculate stop loss based on selected method

get_long_stop_loss_price(base_price) =>

switch stop_loss_method

'PERC' => base_price * (1 - long_stop_loss_percent)

'ATR' => base_price - long_stop_loss_atr_multiplier * entry_atr

'RR' => base_price - (get_long_take_profit_price() - base_price) / long_risk_reward_ratio

=> na

// Implement trailing functionality

strategy.exit(

id = 'Long Take Profit / Stop Loss',

from_entry = 'L',

qty_percent = take_profit_quantity_percent,

limit = trailing_take_profit_enabled ? na : long_take_profit_price,

stop = long_stop_loss_price,

trail_price = trailing_take_profit_enabled ? long_take_profit_price : na,

trail_offset = trailing_take_profit_enabled ? long_trailing_tp_step_ticks : na,

comment = "TP/SL Triggered"

)

This flexible approach adapts to varying market conditions while providing comprehensive downside protection.

Performance Characteristics

Rigorous backtesting demonstrates exceptional capital appreciation potential with impressive risk-adjusted metrics:

Remarkable total return profile (1,517%+)

Strong Sortino ratio (3.691) indicating superior downside risk control

Profit factor of 1.924 across all trades (2.153 for long positions)

Win rate exceeding 35% with balanced distribution across varied market conditions

Institutional Considerations

The strategy architecture addresses execution complexities faced by institutional participants with temporal filtering and date-range capabilities:

// Time Filter settings with flexible timezone support

import jason5480/time_filters/5 as time_filter

src_timezone = input.string(defval = 'Exchange', title = 'Source Timezone')

dst_timezone = input.string(defval = 'Exchange', title = 'Destination Timezone')

// Date range filtering for precise execution windows

use_from_date = input.bool(defval = true, title = 'Enable Start Date')

from_date = input.time(defval = timestamp('01 Jan 2022 00:00'), title = 'Start Date')

// Validate trading permission based on temporal constraints

date_filter_approved = time_filter.is_in_date_range(

use_from_date, from_date, use_to_date, to_date, src_timezone, dst_timezone

)

These capabilities enable precise execution timing and market session optimization critical for larger market participants.

Acknowledgments

Special thanks to LuxAlgo for the pioneering work on trendline detection and breakout identification that inspired elements of this strategy. Their innovative approach to technical analysis provided a valuable foundation upon which I could build my Fibonacci-based methodology.

This strategy is shared under the same Attribution-NonCommercial-ShareAlike 4.0 International (CC BY-NC-SA 4.0) license as LuxAlgo's original work.

Past performance is not indicative of future results. Conduct thorough analysis before implementing any algorithmic strategy.

Search in scripts for "profit factor"

Slight Swing Momentum Strategy.Introduction:

The Swing Momentum Strategy is a quantitative trading strategy designed to capture mid-term opportunities in the financial markets by combining swing trading principles with momentum indicators. It utilizes a combination of technical indicators, including moving averages, crossover signals, and volume analysis, to generate buy and sell signals. The strategy aims to identify market trends and capitalize on price momentum for profit generation.

Highlights:

The strategy offers several key highlights that make it unique and potentially attractive to traders:

Swing Trading with Momentum: The strategy combines the principles of swing trading, which aim to capture short-to-medium-term price swings, with momentum indicators that help identify strong price trends and potential breakout opportunities.

Technical Indicator Optimization: The strategy utilizes a selection of optimized technical indicators, including moving averages and crossover signals, to filter out the noise and focus on high-probability trading setups. This optimization enhances the strategy's ability to identify favourable entry and exit points.

Risk Management: The strategy incorporates risk management techniques, such as position sizing based on equity and dynamic stop loss levels, to manage risk exposure and protect capital. This helps to minimize drawdowns and preserve profits.

Buy Condition:

The buy condition in the strategy is determined by a combination of factors, including A1, A2, A3, XG, and weeklySlope. Let's break it down:

A1 Condition: The A1 condition checks for specific price relationships. It verifies that the ratio of the highest price to the closing price is less than 1.03, the ratio of the opening price to the lowest price is less than 1.03, and the ratio of the highest price to the previous day's closing price is greater than 1.06. This condition looks for a specific pattern indicating potential bullish momentum.

A2 Condition: The A2 condition checks for price relationships related to the closing price. It verifies that the ratio of the closing price to the opening price is greater than 1.05 or that the ratio of the closing price to the previous day's closing price is greater than 1.05. This condition looks for signs of upward price movement and momentum.

A3 Condition: The A3 condition focuses on volume. It checks if the current volume crosses above the highest volume over the last 60 periods. This condition aims to identify increased buying interest and potentially confirms the strength of the potential upward price movement.

XG Condition: The XG condition combines the A1 and A2 conditions and checks if they are true for both the current and previous bars. It also verifies that the ratio of the closing price to the 5-period EMA crosses above the 9-period SMA of the same ratio. This condition helps identify potential buy signals when multiple factors align, indicating a strong bullish momentum and potential entry point.

Weekly Trend Factor: The weekly slope condition calculates the slope of the 50-period SMA over a weekly timeframe. It checks if the slope is positive, indicating an overall upward trend on a weekly basis. This condition provides additional confirmation that the stock is in an upward trend.

When all of these conditions align, the buy condition is triggered, indicating a favourable time to enter a long position.

Sell Condition:

The sell condition is relatively straightforward in the strategy:

Sell Signal: The sell condition simply checks if the closing price crosses below the 10-period EMA. When this condition is met, it indicates a potential reversal or weakening of the upward price momentum, and a sell signal is generated.

Backtest Outcome:

The strategy was backtested over the period from January 22nd, 1999 to May 3rd, 2023, using daily candlestick charts for the NASDAQ: NVDA. The strategy used an initial capital of 1,000,000 USD, The order quantity is defined as 10% of the equity. The strategy allows for pyramiding with 1 order, and the transaction fee is set at 0.03% per trade. Here are the key outcomes of the backtest:

Net Profit: 539,595.84 USD, representing a return of 53.96%.

Percent Profitable: 48.82%

Total Closed Trades: 127

Profit Factor: 2.331

Max Drawdown: 68,422.70 USD

Average Trade: 4,248.79 USD

Average Number of Bars in Trades: 11, indicating the average duration of the trades.

Conclusion:

In conclusion, the Swing Momentum Strategy is a quantitative trading approach that combines swing trading principles with momentum indicators to identify and capture mid term trading opportunities. The strategy has demonstrated promising results during backtesting, including a significant net profit and a favourable profit factor.

Multi Fibonacci Supertrend with Signals【FIbonacciFlux】Multi Fibonacci Supertrend with Signals (MFSS)

Overview

The Multi Fibonacci Supertrend with Signals (MFSS) is an advanced technical analysis tool that combines multiple Supertrend indicators using Fibonacci ratios to identify trend directions and potential trading opportunities.

Key Features

1. Fibonacci-Based Supertrend Levels

* Factor 1 (Weak) : 0.618 - The golden ratio

* Factor 2 (Medium) : 1.618 - The Fibonacci ratio

* Factor 3 (Strong) : 2.618 - The extension ratio

2. Visual Components

* Multi-layered Trend Lines

* Different line weights for easy identification

* Progressive transparency from Factor 1 to Factor 3

* Color-coded trend directions (Green for bullish, Red for bearish)

* Dynamic Fill Areas

* Gradient fills between price and trend lines

* Visual representation of trend strength

* Automatic color adjustment based on trend direction

* Signal Indicators

* Clear BUY/SELL labels on chart

* Position-adaptive signal placement

* High-visibility color scheme

3. Signal Generation Logic

The system generates signals based on two key conditions:

* Primary Condition :

* BUY : Price crossunder Supertrend2 (Factor 1.618)

* SELL : Price crossover Supertrend2 (Factor 1.618)

* Confirmation Filter :

* Signals only trigger when Supertrend3 confirms the trend direction

* Reduces false signals in volatile markets

Technical Details

Input Parameters

* ATR Period : 10 (default)

* Customizable for different market conditions

* Affects sensitivity of all Supertrend levels

* Factor Settings :

* All factors are customizable

* Default values based on Fibonacci sequence

* Minimum value: 0.01

* Step size: 0.01

Alert System

* Built-in alert conditions

* Customizable alert messages

* Real-time notification support

Use Cases

* Trend Trading

* Identify strong trend directions

* Filter out weak signals

* Confirm trend continuations

* Risk Management

* Multiple trend levels for stop-loss placement

* Clear entry and exit signals

* Trend strength visualization

* Market Analysis

* Multi-timeframe analysis capability

* Trend strength assessment

* Market structure identification

Benefits

* Reliability

* Based on proven Supertrend algorithm

* Enhanced with Fibonacci mathematics

* Multiple confirmation levels

* Clarity

* Clear visual signals

* Easy-to-interpret interface

* Reduced noise in signal generation

* Flexibility

* Customizable parameters

* Adaptable to different markets

* Suitable for various trading styles

Performance Considerations

* Optimized code structure

* Efficient calculation methods

* Minimal resource usage

Installation and Usage

Setup

* Add indicator to chart

* Adjust parameters if needed

* Enable alerts as required

Best Practices

* Use with other confirmation tools

* Adjust factors based on market volatility

* Consider timeframe appropriateness

Backtesting Results and Strategy Performance

This indicator is specifically designed for pullback trading with optimized risk-reward ratios in trend-following strategies. Below are the detailed backtesting results from our proprietary strategy implementation:

BTCUSDT Performance (Binance)

* Test Period: Approximately 7 years

* Risk-Reward Ratio: 2:1

* Take Profit: 8%

* Stop Loss: 4%

Key Metrics (BTCUSDT):

* Net Profit: +2,579%

* Total Trades: 551

* Win Rate: 44.8%

* Profit Factor: 1.278

* Maximum Drawdown: 42.86%

ETHUSD Performance (Binance)

* Risk-Reward Ratio: 4.33:1

* Take Profit: 13%

* Stop Loss: 3%

Key Metrics (ETHUSD):

* Net Profit: +8,563%

* Total Trades: 581

* Win Rate: 32%

* Profit Factor: 1.32

* Maximum Drawdown: 55%

Strategy Highlights:

* Optimized for pullback trading in strong trends

* Focus on high risk-reward ratios

* Proven effectiveness in major cryptocurrency pairs

* Consistent performance across different market conditions

* Robust profit factor despite moderate win rates

Note: These results are from our proprietary strategy implementation and should be used as reference only. Individual results may vary based on market conditions and implementation.

Important Considerations:

* The strategy demonstrates strong profitability despite lower win rates, emphasizing the importance of proper risk-reward ratios

* Higher drawdowns are compensated by significant overall returns

* The system shows adaptability across different cryptocurrencies with consistent profit factors

* Results suggest optimal performance in volatile crypto markets

Real Trading Examples

BTCUSDT 4-Hour Chart Analysis

Example of pullback strategy implementation on Bitcoin, showing clear trend definition and entry points

ETHUSDT 4-Hour Chart Analysis

Ethereum chart demonstrating effective signal generation during strong trends

BTCUSDT Detailed Signal Example (15-Minute Scalping)

Close-up view of signal generation and trend confirmation process on 15-minute timeframe, demonstrating the indicator's effectiveness for scalping operations

Chart Analysis Notes:

* Green and red zones clearly indicate trend direction

* Multiple timeframe confirmation visible through different Supertrend levels

* Clear entry signals during pullbacks in established trends

* Precise stop-loss placement opportunities below support levels

Implementation Guidelines:

* Wait for main trend confirmation from Factor 3 (2.618)

* Enter trades on pullbacks to Factor 2 (1.618)

* Use Factor 1 (0.618) for fine-tuning entry points

* Place stops below the relevant Supertrend level

Footnotes:

* Charts provided are from Binance exchange, using both 4-hour and 15-minute timeframes

* Trading view screenshots captured during actual market conditions

* Indicators shown: Multi Fibonacci Supertrend with all three factors

* Time period: Recent market activity showing various market conditions

Important Notice:

These charts are for educational purposes only. Past performance does not guarantee future results. Always conduct your own analysis and risk management.

Disclaimer

This indicator is for informational purposes only. Past performance is not indicative of future results. Always conduct proper risk management and due diligence.

License

Open source under MIT License

Author's Note

Contributions and suggestions for improvement are welcome. Please feel free to fork and enhance.

Golden Cross 50/200 EMATrend-following systems are characterized by having a low win rate, yet in the right circumstances (trending markets and higher timeframes) they can deliver returns that even surpass those of systems with a high win rate.

Below, I show you a simple bullish trend-following system with clear execution rules:

System Rules

-Long entries when the 50-period EMA crosses above the 200-period EMA.

-Stop Loss (SL) placed at the lowest low of the 15 candles prior to the entry candle.

-Take Profit (TP) triggered when the 50-period EMA crosses below the 200-period EMA.

Risk Management

-Initial capital: $10,000

-Position size: 10% of capital per trade

-Commissions: 0.1% per trade

Important Note:

In the code, the stop loss is defined using the swing low (15 candles), but the position size is not adjusted based on the distance to the stop loss. In other words, 10% of the equity is risked on each trade, but the actual loss on the trade is not controlled by a maximum fixed percentage of the account — it depends entirely on the stop loss level. This means the loss on a single trade could be significantly higher or lower than 10% of the account equity, depending on volatility.

Implementing leverage or reducing position size based on volatility is something I haven’t been able to include in the code, but it would dramatically improve the system’s performance. It would fix a consistent percentage loss per trade, preventing losses from fluctuating wildly with changes in volatility.

For example, we can maintain a fixed loss percentage when volatility is low by using the following formula:

Leverage = % of SL you’re willing to risk / % volatility from entry point to stop loss

And when volatility is high and would exceed the fixed percentage we want to expose per trade (if the SL is hit), we could reduce the position size accordingly.

Practical example:

Imagine we only want to risk 15% of the position value if the stop loss is triggered on Tesla (which has high volatility), but the distance to the SL represents a potential 23.57% drop. In this case, we subtract the desired risk (15%) from the actual volatility-based loss (23.57%):

23.57% − 15% = 8.57%

Now suppose we normally use $200 per trade.

To calculate 8.57% of $200:

200 × (8.57 / 100) = $17.14

Then subtract that amount from the original position size:

$200 − $17.14 = $182.86

In summary:

If we reduce the position size to $182.86 (instead of the usual $200), even if Tesla moves 23.57% against us and hits the stop loss, we would still only lose approximately 15% of the original $200 position — exactly the risk level we defined. This way, we strictly respect our risk management rules regardless of volatility swings.

I hope this clearly explains the importance of capping losses at a fixed percentage per trade. This keeps risk under control while maintaining a consistent percentage of capital invested per trade — preventing both statistical distortion of the system and the potential destruction of the account.

About the code:

Strategy declaration:

The strategy is named 'Golden Cross 50/200 EMA'.

overlay=true means it will be drawn directly on the price chart.

initial_capital=10000 sets the initial capital to $10,000.

default_qty_type=strategy.percent_of_equity and default_qty_value=10 means each trade uses 10% of available equity.

margin_long=0 indicates no margin is used for long positions (this is likely for simulation purposes only; in real trading, margin would be required).

commission_type=strategy.commission.percent and commission_value=0.1 sets a 0.1% commission per trade.

Indicators:

Calculates two EMAs: a 50-period EMA (ema50) and a 200-period EMA (ema200).

Crossover detection:

bullCross is triggered when the 50-period EMA crosses above the 200-period EMA (Golden Cross).

bearCross is triggered when the 50-period EMA crosses below the 200-period EMA (Death Cross).

Recent swing:

swingLow calculates the lowest low of the previous 15 periods.

Stop Loss:

entryStopLoss is a variable initialized as na (not available) and is updated to the current swingLow value whenever a bullCross occurs.

Entry and exit conditions:

Entry: When a bullCross occurs, the initial stop loss is set to the current swingLow and a long position is opened.

Exit on opposite signal: When a bearCross occurs, the long position is closed.

Exit on stop loss: If the price falls below entryStopLoss while a position is open, the position is closed.

Visualization:

Both EMAs are plotted (50-period in blue, 200-period in red).

Green triangles are plotted below the bar on a bullCross, and red triangles above the bar on a bearCross.

A horizontal orange line is drawn that shows the stop loss level whenever a position is open.

Alerts:

Alerts are created for:Long entry

Exit on bearish crossover (Death Cross)

Exit triggered by stop loss

Favorable Conditions:

Tesla (45-minute timeframe)

June 29, 2010 – November 17, 2025

Total net profit: $12,458.73 or +124.59%

Maximum drawdown: $1,210.40 or 8.29%

Total trades: 107

Winning trades: 27.10% (29/107)

Profit factor: 3.141

Tesla (1-hour timeframe)

June 29, 2010 – November 17, 2025

Total net profit: $7,681.83 or +76.82%

Maximum drawdown: $993.36 or 7.30%

Total trades: 75

Winning trades: 29.33% (22/75)

Profit factor: 3.157

Netflix (45-minute timeframe)

May 23, 2002 – November 17, 2025

Total net profit: $11,380.73 or +113.81%

Maximum drawdown: $699.45 or 5.98%

Total trades: 134

Winning trades: 36.57% (49/134)

Profit factor: 2.885

Netflix (1-hour timeframe)

May 23, 2002 – November 17, 2025

Total net profit: $11,689.05 or +116.89%

Maximum drawdown: $844.55 or 7.24%

Total trades: 107

Winning trades: 37.38% (40/107)

Profit factor: 2.915

Netflix (2-hour timeframe)

May 23, 2002 – November 17, 2025

Total net profit: $12,807.71 or +128.10%

Maximum drawdown: $866.52 or 6.03%

Total trades: 56

Winning trades: 41.07% (23/56)

Profit factor: 3.891

Meta (45-minute timeframe)

May 18, 2012 – November 17, 2025

Total net profit: $2,370.02 or +23.70%

Maximum drawdown: $365.27 or 3.50%

Total trades: 83

Winning trades: 31.33% (26/83)

Profit factor: 2.419

Apple (45-minute timeframe)

January 3, 2000 – November 17, 2025

Total net profit: $8,232.55 or +80.59%

Maximum drawdown: $581.11 or 3.16%

Total trades: 140

Winning trades: 34.29% (48/140)

Profit factor: 3.009

Apple (1-hour timeframe)

January 3, 2000 – November 17, 2025

Total net profit: $9,685.89 or +94.93%

Maximum drawdown: $374.69 or 2.26%

Total trades: 118

Winning trades: 35.59% (42/118)

Profit factor: 3.463

Apple (2-hour timeframe)

January 3, 2000 – November 17, 2025

Total net profit: $8,001.28 or +77.99%

Maximum drawdown: $755.84 or 7.56%

Total trades: 67

Winning trades: 41.79% (28/67)

Profit factor: 3.825

NVDA (15-minute timeframe)

January 3, 2000 – November 17, 2025

Total net profit: $11,828.56 or +118.29%

Maximum drawdown: $1,275.43 or 8.06%

Total trades: 466

Winning trades: 28.11% (131/466)

Profit factor: 2.033

NVDA (30-minute timeframe)

January 3, 2000 – November 17, 2025

Total net profit: $12,203.21 or +122.03%

Maximum drawdown: $1,661.86 or 10.35%

Total trades: 245

Winning trades: 28.98% (71/245)

Profit factor: 2.291

NVDA (45-minute timeframe)

January 3, 2000 – November 17, 2025

Total net profit: $16,793.48 or +167.93%

Maximum drawdown: $1,458.81 or 8.40%

Total trades: 172

Winning trades: 33.14% (57/172)

Profit factor: 2.927

888 BOT #backtest█ 888 BOT #backtest (open source)

This is an Expert Advisor 'EA' or Automated trading script for ‘longs’ and ‘shorts’, which uses only a Take Profit or, in the worst case, a Stop Loss to close the trade.

It's a much improved version of the previous ‘Repanocha’. It doesn`t use 'Trailing Stop' or 'security()' functions (although using a security function doesn`t mean that the script repaints) and all signals are confirmed, therefore the script doesn`t repaint in alert mode and is accurate in backtest mode.

Apart from the previous indicators, some more and other functions have been added for Stop-Loss, re-entry and leverage.

It uses 8 indicators, (many of you already know what they are, but in case there is someone new), these are the following:

1. Jurik Moving Average

It's a moving average created by Mark Jurik for professionals which eliminates the 'lag' or delay of the signal. It's better than other moving averages like EMA , DEMA , AMA or T3.

There are two ways to decrease noise using JMA . Increasing the 'LENGTH' parameter will cause JMA to move more slowly and therefore reduce noise at the expense of adding 'lag'

The 'JMA LENGTH', 'PHASE' and 'POWER' parameters offer a way to select the optimal balance between 'lag' and over boost.

Green: Bullish , Red: Bearish .

2. Range filter

Created by Donovan Wall, its function is to filter or eliminate noise and to better determine the price trend in the short term.

First, a uniform average price range 'SAMPLING PERIOD' is calculated for the filter base and multiplied by a specific quantity 'RANGE MULTIPLIER'.

The filter is then calculated by adjusting price movements that do not exceed the specified range.

Finally, the target ranges are plotted to show the prices that will trigger the filter movement.

Green: Bullish , Red: Bearish .

3. Average Directional Index ( ADX Classic) and ( ADX Masanakamura)

It's an indicator designed by Welles Wilder to measure the strength and direction of the market trend. The price movement is strong when the ADX has a positive slope and is above a certain minimum level 'ADX THRESHOLD' and for a given period 'ADX LENGTH'.

The green color of the bars indicates that the trend is bullish and that the ADX is above the level established by the threshold.

The red color of the bars indicates that the trend is down and that the ADX is above the threshold level.

The orange color of the bars indicates that the price is not strong and will surely lateralize.

You can choose between the classic option and the one created by a certain 'Masanakamura'. The main difference between the two is that in the first it uses RMA () and in the second SMA () in its calculation.

4. Parabolic SAR

This indicator, also created by Welles Wilder, places points that help define a trend. The Parabolic SAR can follow the price above or below, the peculiarity that it offers is that when the price touches the indicator, it jumps to the other side of the price (if the Parabolic SAR was below the price it jumps up and vice versa) to a distance predetermined by the indicator. At this time the indicator continues to follow the price, reducing the distance with each candle until it is finally touched again by the price and the process starts again. This procedure explains the name of the indicator: the Parabolic SAR follows the price generating a characteristic parabolic shape, when the price touches it, stops and turns ( SAR is the acronym for 'stop and reverse'), giving rise to a new cycle. When the points are below the price, the trend is up, while the points above the price indicate a downward trend.

5. RSI with Volume

This indicator was created by LazyBear from the popular RSI .

The RSI is an oscillator-type indicator used in technical analysis and also created by Welles Wilder that shows the strength of the price by comparing individual movements up or down in successive closing prices.

LazyBear added a volume parameter that makes it more accurate to the market movement.

A good way to use RSI is by considering the 50 'RSI CENTER LINE' centerline. When the oscillator is above, the trend is bullish and when it is below, the trend is bearish .

6. Moving Average Convergence Divergence ( MACD ) and ( MAC-Z )

It was created by Gerald Appel. Subsequently, the histogram was added to anticipate the crossing of MA. Broadly speaking, we can say that the MACD is an oscillator consisting of two moving averages that rotate around the zero line. The MACD line is the difference between a short moving average 'MACD FAST MA LENGTH' and a long moving average 'MACD SLOW MA LENGTH'. It's an indicator that allows us to have a reference on the trend of the asset on which it is operating, thus generating market entry and exit signals.

We can talk about a bull market when the MACD histogram is above the zero line, along with the signal line, while we are talking about a bear market when the MACD histogram is below the zero line.

There is the option of using the MAC-Z indicator created by LazyBear, which according to its author is more effective, by using the parameter VWAP ( volume weighted average price ) 'Z-VWAP LENGTH' together with a standard deviation 'STDEV LENGTH' in its calculation.

7. Volume Condition

Volume indicates the number of participants in this war between bulls and bears, the more volume the more likely the price will move in favor of the trend. A low trading volume indicates a lower number of participants and interest in the instrument in question. Low volumes may reveal weakness behind a price movement.

With this condition, those signals whose volume is less than the volume SMA for a period 'SMA VOLUME LENGTH' multiplied by a factor 'VOLUME FACTOR' are filtered. In addition, it determines the leverage used, the more volume , the more participants, the more probability that the price will move in our favor, that is, we can use more leverage. The leverage in this script is determined by how many times the volume is above the SMA line.

The maximum leverage is 8.

8. Bollinger Bands

This indicator was created by John Bollinger and consists of three bands that are drawn superimposed on the price evolution graph.

The central band is a moving average, normally a simple moving average calculated with 20 periods is used. ('BB LENGTH' Number of periods of the moving average)

The upper band is calculated by adding the value of the simple moving average X times the standard deviation of the moving average. ('BB MULTIPLIER' Number of times the standard deviation of the moving average)

The lower band is calculated by subtracting the simple moving average X times the standard deviation of the moving average.

the band between the upper and lower bands contains, statistically, almost 90% of the possible price variations, which means that any movement of the price outside the bands has special relevance.

In practical terms, Bollinger bands behave as if they were an elastic band so that, if the price touches them, it has a high probability of bouncing.

Sometimes, after the entry order is filled, the price is returned to the opposite side. If price touch the Bollinger band in the same previous conditions, another order is filled in the same direction of the position to improve the average entry price, (% MINIMUM BETTER PRICE ': Minimum price for the re-entry to be executed and that is better than the price of the previous position in a given %) in this way we give the trade a chance that the Take Profit is executed before. The downside is that the position is doubled in size. 'ACTIVATE DIVIDE TP': Divide the size of the TP in half. More probability of the trade closing but less profit.

█ STOP LOSS and RISK MANAGEMENT.

A good risk management is what can make your equity go up or be liquidated.

The % risk is the percentage of our capital that we are willing to lose by operation. This is recommended to be between 1-5%.

% Risk: (% Stop Loss x % Equity per trade x Leverage) / 100

First the strategy is calculated with Stop Loss, then the risk per operation is determined and from there, the amount per operation is calculated and not vice versa.

In this script you can use a normal Stop Loss or one according to the ATR. Also activate the option to trigger it earlier if the risk percentage is reached. '% RISK ALLOWED'

'STOP LOSS CONFIRMED': The Stop Loss is only activated if the closing of the previous bar is in the loss limit condition. It's useful to prevent the SL from triggering when they do a ‘pump’ to sweep Stops and then return the price to the previous state.

█ BACKTEST

The objective of the Backtest is to evaluate the effectiveness of our strategy. A good Backtest is determined by some parameters such as:

- RECOVERY FACTOR: It consists of dividing the 'net profit' by the 'drawdown’. An excellent trading system has a recovery factor of 10 or more; that is, it generates 10 times more net profit than drawdown.

- PROFIT FACTOR: The ‘Profit Factor’ is another popular measure of system performance. It's as simple as dividing what win trades earn by what loser trades lose. If the strategy is profitable then by definition the 'Profit Factor' is going to be greater than 1. Strategies that are not profitable produce profit factors less than one. A good system has a profit factor of 2 or more. The good thing about the ‘Profit Factor’ is that it tells us what we are going to earn for each dollar we lose. A profit factor of 2.5 tells us that for every dollar we lose operating we will earn 2.5.

- SHARPE: (Return system - Return without risk) / Deviation of returns.

When the variations of gains and losses are very high, the deviation is very high and that leads to a very poor ‘Sharpe’ ratio. If the operations are very close to the average (little deviation) the result is a fairly high 'Sharpe' ratio. If a strategy has a 'Sharpe' ratio greater than 1 it is a good strategy. If it has a 'Sharpe' ratio greater than 2, it is excellent. If it has a ‘Sharpe’ ratio less than 1 then we don't know if it is good or bad, we have to look at other parameters.

- MATHEMATICAL EXPECTATION: (% winning trades X average profit) + (% losing trades X average loss).

To earn money with a Trading system, it is not necessary to win all the operations, what is really important is the final result of the operation. A Trading system has to have positive mathematical expectation as is the case with this script: ME = (0.87 x 30.74$) - (0.13 x 56.16$) = (26.74 - 7.30) = 19.44$ > 0

The game of roulette, for example, has negative mathematical expectation for the player, it can have positive winning streaks, but in the long term, if you continue playing you will end up losing, and casinos know this very well.

PARAMETERS

'BACKTEST DAYS': Number of days back of historical data for the calculation of the Backtest.

'ENTRY TYPE': For '% EQUITY' if you have $ 10,000 of capital and select 7.5%, for example, your entry would be $ 750 without leverage. If you select CONTRACTS for the 'BTCUSDT' pair, for example, it would be the amount in 'Bitcoins' and if you select 'CASH' it would be the amount in $ dollars.

'QUANTITY (LEVERAGE 1X)': The amount for an entry with X1 leverage according to the previous section.

'MAXIMUM LEVERAGE': It's the maximum allowed multiplier of the quantity entered in the previous section according to the volume condition.

The settings are for Bitcoin at Binance Futures (BTC: USDTPERP) in 15 minutes.

For other pairs and other timeframes, the settings have to be adjusted again. And within a month, the settings will be different because we all know the market and the trend are changing.

Vital Wave 20-50Simplicity is almost always the most effective approach, and here I’m giving you a trend-following system that exploits the bullish bias of traditional markets and their trending nature, with very basic rules.

Rules (long entries only)

• Market entry: When the EMA 20 crosses above the EMA 50 (from below)

• Main market exit: When the EMA 20 crosses below the EMA 50 (from above)

• Fixed Stop Loss: Placed at the price level of the Lower Bollinger Band at the moment the trade is entered.

In my strategy, the primary exit is when the EMA 20 crosses below the EMA 50. However, this crossover can sometimes take a while to occur, and in the meantime the price may have already dropped significantly. The Stop Loss based on the Lower Bollinger Band is designed to limit losses in case the market moves sharply against the position without giving the bearish crossover signal in time. Having two exit conditions makes the strategy much more robust in terms of risk management.

Risk Management:

• Initial capital: $10,000

• Position size: 10% of available capital per trade

• Commissions: 0.1% on traded volume

• Stop Loss: Based on the Lower Bollinger Band

• Take Profit / Exit: When EMA 20 crosses below EMA 50

Recommended Markets:

XAUUSD (OANDA) (Daily)

Period: January 3, 1833 – November 23, 2025

Total Profit & Loss: +$6,030.62 USD (+57.57%)

Maximum Drawdown: $541.53 USD (3.83%)

Total Trades: 136

Winning Trades (Win Rate): 36.03% (49/136)

Profit Factor: 2.483

XAUUSD (OANDA) (12-hour)

Period: March 19, 2006 – November 23, 2025

Total Profit & Loss: +$1,209.56 USD (+11.89%)

Maximum Drawdown: $384.58 USD (3.61%)

Total Trades: 97

Winning Trades (Win Rate): 35.05% (34/97)

Profit Factor: 1.676

XAUUSD (OANDA) (8-hour)

Period: March 19, 2006 – November 23, 2025

Total Profit & Loss: +$1,179.36 USD (+11.81%)

Maximum Drawdown: $246.88 USD (2.32%)

Total Trades: 147

Winning Trades (Win Rate): 31.97% (47/147)

Profit Factor: 1.626

Tesla (NASDAQ) (4-hour)

Period: June 29, 2010 – November 23, 2025

Total Profit & Loss (Absolute): +$11,687.90 USD (+116.88%)

Maximum Drawdown: $922.05 USD (6.50%)

Total Trades: 68

Winning Trades (Win Rate): 39.71% (27/68)

Profit Factor: 4.156

Tesla (NASDAQ) (3-hour)

Total Profit & Loss: +$11,522.33 USD (+115.22%)

Maximum Drawdown: $1,247.60 USD (8.80%)

Total Trades: 114

Winning Trades: 33.33% (38/114)

Profit Factor: 2.811

Additional Recommendations

(These assets have shown good trending behavior with the same strategy across multiple timeframes):

• NVDA (15 min, 30 min, 1h, 2h, 3h, 4h, 6h, 8h, 12h, Daily)

• NFLX (1h, 2h, 3h, 4h, 6h, 8h, 12h, Daily)

• MA (1h, 2h, 3h, 4h, 6h, 8h, 12h, Daily)

• META (1h, 2h, 3h, 4h, 6h, 8h, 12h, Daily)

• AAPL (1h, 2h, 3h, 4h, 6h, 8h, 12h, Daily)

• SPY (12h, Daily)

About the Code

The user can modify:

• EMA periods (20 and 50 by default)

• Bollinger Bands length (20 periods)

• Standard deviation (2.0)

Visualization

• EMA 20: Blue line

• EMA 50: Red line

• Green background when EMA20 > EMA50 (bullish trend)

• Red background when EMA20 < EMA50 (bearish trend)

Important Note:

We can significantly increase the profit factor and overall profitability by risking a fixed percentage per trade instead of a fixed amount. This would prevent losses from fluctuating with changes in volatility.

This could be implemented by reducing position size or adjusting leverage based on the volatility percentage required for each trade, but I’m not sure if this is fully possible in Pine Script. In my other script, “ Golden Cross 50/200 EMA ,” I go deeper into this topic and provide examples.

I hope you enjoy this contribution. Best regards!

BullBear with Volume-Percentile TP - Strategy [presentTrading] Happy New Year, everyone! I hope we have a fantastic year ahead.

It's been a while since I published an open script, but it's time to return.

This strategy introduces an indicator called Bull Bear Power, combined with an advanced take-profit system, which is the main innovative and educational aspect of this script. I hope all of you find some useful insights here. Welcome to engage in meaningful exchanges. This is a versatile tool suitable for both novice and experienced traders.

█ Introduction and How it is Different

Unlike traditional strategies that rely solely on price or volume indicators, this approach combines Bull Bear Power (BBP) with volume percentile analysis to identify optimal entry and exit points. It features a dynamic take-profit mechanism based on ATR (Average True Range) multipliers adjusted by volume and percentile factors, ensuring adaptability to diverse market conditions. This multifaceted strategy not only improves signal accuracy but also optimizes risk management, distinguishing it from conventional trading methods.

BTCUSD 6hr performance

Disable the visualization of Bull Bear Power (BBP) to clearly view the Z-Score.

█ Strategy, How it Works: Detailed Explanation

The BBP Strategy with Volume-Percentile TP utilizes several interconnected components to analyze market data and generate trading signals. Here's an overview with essential equations:

🔶 Core Indicators and Calculations

1. Exponential Moving Average (EMA):

- **Purpose:** Smoothens price data to identify trends.

- **Formula:**

EMA_t = (Close_t * (2 / (lengthInput + 1))) + (EMA_(t-1) * (1 - (2 / (lengthInput + 1))))

- Usage: Baseline for Bull and Bear Power.

2. Bull and Bear Power:

- Bull Power: `BullPower = High_t - EMA_t`

- Bear Power: `BearPower = Low_t - EMA_t`

- BBP:** `BBP = BullPower + BearPower`

- Interpretation: Positive BBP indicates bullish strength, negative indicates bearish.

3. Z-Score Calculation:

- Purpose: Normalizes BBP to assess deviation from the mean.

- Formula:

Z-Score = (BBP_t - bbp_mean) / bbp_std

- Components:

- `bbp_mean` = SMA of BBP over `zLength` periods.

- `bbp_std` = Standard deviation of BBP over `zLength` periods.

- Usage: Identifies overbought or oversold conditions based on thresholds.

🔶 Volume Analysis

1. Volume Moving Average (`vol_sma`):

vol_sma = (Volume_1 + Volume_2 + ... + Volume_vol_period) / vol_period

2. Volume Multiplier (`vol_mult`):

vol_mult = Current Volume / vol_sma

- Thresholds:

- High Volume: `vol_mult > 2.0`

- Medium Volume: `1.5 < vol_mult ≤ 2.0`

- Low Volume: `1.0 < vol_mult ≤ 1.5`

🔶 Percentile Analysis

1. Percentile Calculation (`calcPercentile`):

Percentile = (Number of values ≤ Current Value / perc_period) * 100

2. Thresholds:

- High Percentile: >90%

- Medium Percentile: >80%

- Low Percentile: >70%

🔶 Dynamic Take-Profit Mechanism

1. ATR-Based Targets:

TP1 Price = Entry Price ± (ATR * atrMult1 * TP_Factor)

TP2 Price = Entry Price ± (ATR * atrMult2 * TP_Factor)

TP3 Price = Entry Price ± (ATR * atrMult3 * TP_Factor)

- ATR Calculation:

ATR_t = (True Range_1 + True Range_2 + ... + True Range_baseAtrLength) / baseAtrLength

2. Adjustment Factors:

TP_Factor = (vol_score + price_score) / 2

- **vol_score** and **price_score** are based on current volume and price percentiles.

Local performance

🔶 Entry and Exit Logic

1. Long Entry: If Z-Score crosses above 1.618, then Enter Long.

2. Short Entry: If Z-Score crosses below -1.618, then Enter Short.

3. Exiting Positions:

If Long and Z-Score crosses below 0:

Exit Long

If Short and Z-Score crosses above 0:

Exit Short

4. Take-Profit Execution:

- Set multiple exit orders at dynamically calculated TP levels based on ATR and adjusted by `TP_Factor`.

█ Trade Direction

The strategy determines trade direction using the Z-Score from the BBP indicator:

- Long Positions:

- Condition: Z-Score crosses above 1.618.

- Short Positions:

- Condition: Z-Score crosses below -1.618.

- Exiting Trades:

- Long Exit: Z-Score drops below 0.

- Short Exit: Z-Score rises above 0.

This approach aligns trades with prevailing market trends, increasing the likelihood of successful outcomes.

█ Usage

Implementing the BBP Strategy with Volume-Percentile TP in TradingView involves:

1. Adding the Strategy:

- Copy the Pine Script code.

- Paste it into TradingView's Pine Editor.

- Save and apply the strategy to your chart.

2. Configuring Settings:

- Adjust parameters like EMA length, Z-Score thresholds, ATR multipliers, volume periods, and percentile settings to match your trading preferences and asset behavior.

3. Backtesting:

- Use TradingView’s backtesting tools to evaluate historical performance.

- Analyze metrics such as profit factor, drawdown, and win rate.

4. Optimization:

- Fine-tune parameters based on backtesting results.

- Test across different assets and timeframes to enhance adaptability.

5. Deployment:

- Apply the strategy in a live trading environment.

- Continuously monitor and adjust settings as market conditions change.

█ Default Settings

The BBP Strategy with Volume-Percentile TP includes default parameters designed for balanced performance across various markets. Understanding these settings and their impact is essential for optimizing strategy performance:

Bull Bear Power Settings:

- EMA Length (`lengthInput`): 21

- **Effect:** Balances sensitivity and trend identification; shorter lengths respond quicker but may generate false signals.

- Z-Score Length (`zLength`): 252

- **Effect:** Long period for stable mean and standard deviation, reducing false signals but less responsive to recent changes.

- Z-Score Threshold (`zThreshold`): 1.618

- **Effect:** Higher threshold filters out weaker signals, focusing on significant market moves.

Take Profit Settings:

- Use Take Profit (`useTP`): Enabled (`true`)

- **Effect:** Activates dynamic profit-taking, enhancing profitability and risk management.

- ATR Period (`baseAtrLength`): 20

- **Effect:** Shorter period for sensitive volatility measurement, allowing tighter profit targets.

- ATR Multipliers:

- **Effect:** Define conservative to aggressive profit targets based on volatility.

- Position Sizes:

- **Effect:** Diversifies profit-taking across multiple levels, balancing risk and reward.

Volume Analysis Settings:

- Volume MA Period (`vol_period`): 100

- **Effect:** Longer period for stable volume average, reducing the impact of short-term spikes.

- Volume Multipliers:

- **Effect:** Determines volume conditions affecting take-profit adjustments.

- Volume Factors:

- **Effect:** Adjusts ATR multipliers based on volume strength.

Percentile Analysis Settings:

- Percentile Period (`perc_period`): 100

- **Effect:** Balances historical context with responsiveness to recent data.

- Percentile Thresholds:

- **Effect:** Defines price and volume percentile levels influencing take-profit adjustments.

- Percentile Factors:

- **Effect:** Modulates ATR multipliers based on price percentile strength.

Impact on Performance:

- EMA Length: Shorter EMAs increase sensitivity but may cause more false signals; longer EMAs provide stability but react slower to market changes.

- Z-Score Parameters:*Longer Z-Score periods create more stable signals, while higher thresholds reduce trade frequency but increase signal reliability.

- ATR Multipliers and Position Sizes: Higher multipliers allow for larger profit targets with increased risk, while diversified position sizes help in securing profits at multiple levels.

- Volume and Percentile Settings: These adjustments ensure that take-profit targets adapt to current market conditions, enhancing flexibility and performance across different volatility environments.

- Commission and Slippage: Accurate settings prevent overestimation of profitability and ensure the strategy remains viable after accounting for trading costs.

Conclusion

The BBP Strategy with Volume-Percentile TP offers a robust framework by combining BBP indicators with volume and percentile analyses. Its dynamic take-profit mechanism, tailored through ATR adjustments, ensures that traders can effectively capture profits while managing risks in varying market conditions.

Optimized Zhaocaijinbao strategyIntroduction:

The Optimized Zhaocaijinbao strategy is a mid and long-term quantitative trading strategy that combines momentum and trend factors. It generates buy and sell signals by using a combination of exponential moving averages, moving averages, volume and slope indicators. It generates buy signals when the stock is above the 35-day moving average, the trading volume is higher than the 20-day moving average, and the stock is in an upward trend on a weekly timeframe."招财进宝" is a Chinese phrase that can be translated to "Attract Wealth and Bring in Treasure" in English. It is a common expression used to wish for good luck and prosperity in various contexts, such as in business or personal finances.

Highlights:

The strategy has several special optimizations that make it unique.

Firstly, the strategy is optimized for T+1 trading in the Chinese stock market and is only suitable for long positions. The optimizations are also applicable to international stock markets.

Secondly, the trend strategy is optimized to only show indicators on the right side and oscillations. This helps to prevent false signals in choppy markets.

Thirdly, the strategy uses a risk factor for dynamic position sizing to ensure position sizes are adjusted according to the current net asset value and risk preferences. This helps to lower drawdown risks.

The strategy has good resilience even without using stop loss modules in backtesting, making it suitable for trading hourly, 2-hourly, and daily K-line charts (depending on the stock being traded). We recommend experimenting with backtesting using SSE 1-hour or 2-hour or daily Kline charts.

Backtesting outcomes:

The strategy was backtested over the period from October 13th, 2005 to April 14th, 2023, using daily candlestick charts for the commodity code SSE:600763, with a currency of CNY and tick size of 0.01. The strategy used an initial capital of 1,000,000 CNY, with order sizes set to 10% equity and a pyramid of 1 order. The strategy also had a Max Position Size of 0.01 and a Risk Factor of 2.

Here is a summary of the performance of the trading strategy:

Total net profit: 288,577.32 CNY, representing a return of 128.86%

Total number of closed trades: 61

Winning trades: 37, representing a win rate of 60.66%

Profit factor: 2.415

Largest losing trade: 222,021.46 CNY, representing a loss of 14.08%

Average trade: 21,124.22 CNY, representing a return of 3.1%

Average holding period for all trades: 12 days

Conclusion:

In conclusion, the Optimized Zhaocaijinbao strategy is a mid and long-term quantitative trading strategy that combines momentum and trend factors. It is suitable for both Chinese stocks and global stocks. While the Optimized Zhaocaijinbao strategy has performed well in backtesting, it is important to note that past performance is not a guarantee of future results. Traders should conduct their own research and analysis and exercise caution when using any trading strategy.

TitanGrid L/S SuperEngineTitanGrid L/S SuperEngine

Experimental Trend-Aligned Grid Signal Engine for Long & Short Execution

🔹 Overview

TitanGrid is an advanced, real-time signal engine built around a tactical grid structure.

It manages Long and Short trades using trend-aligned entries, layered scaling, and partial exits.

Unlike traditional strategy() -based scripts, TitanGrid runs as an indicator() , but includes its own full internal simulation engine.

This allows it to track capital, equity, PnL, risk exposure, and trade performance bar-by-bar — effectively simulating a custom backtest, while remaining compatible with real-time alert-based execution systems.

The concept was born from the fusion of two prior systems:

Assassin’s Grid (grid-based execution and structure) + Super 8 (trend-filtering, smart capital logic), both developed under the AssassinsGrid framework.

🔹 Disclaimer

This is an experimental tool intended for research, testing, and educational use.

It does not provide guaranteed outcomes and should not be interpreted as financial advice.

Use with demo or simulated accounts before considering live deployment.

🔹 Execution Logic

Trend direction is filtered through a custom SuperTrend engine. Once confirmed:

• Long entries trigger on pullbacks, exiting progressively as price moves up

• Short entries trigger on rallies, exiting as price declines

Grid levels are spaced by configurable percentage width, and entries scale dynamically.

🔹 Stop Loss Mechanism

TitanGrid uses a dual-layer stop system:

• A static stop per entry, placed at a fixed percentage distance matching the grid width

• A trend reversal exit that closes the entire position if price crosses the SuperTrend in the opposite direction

Stops are triggered once per cycle, ensuring predictable and capital-aware behavior.

🔹 Key Features

• Dual-side grid logic (Long-only, Short-only, or Both)

• SuperTrend filtering to enforce directional bias

• Adjustable grid spacing, scaling, and sizing

• Static and dynamic stop-loss logic

• Partial exits and reset conditions

• Webhook-ready alerts (browser-based automation compatible)

• Internal simulation of equity, PnL, fees, and liquidation levels

• Real-time dashboard for full transparency

🔹 Best Use Cases

TitanGrid performs best in structured or mean-reverting environments.

It is especially well-suited to assets with the behavioral profile of ETH — reactive, trend-intraday, and prone to clean pullback formations.

While adaptable to multiple timeframes, it shows strongest performance on the 15-minute chart , offering a balance of signal frequency and directional clarity.

🔹 License

Published under the Mozilla Public License 2.0 .

You are free to study, adapt, and extend this script.

🔹 Panel Reference

The real-time dashboard displays performance metrics, capital state, and position behavior:

• Asset Type – Automatically detects the instrument class (e.g., Crypto, Stock, Forex) from symbol metadata

• Equity – Total simulated capital: realized PnL + floating PnL + remaining cash

• Available Cash – Capital not currently allocated to any position

• Used Margin – Capital locked in open trades, based on position size and leverage

• Net Profit – Realized gain/loss after commissions and fees

• Raw Net Profit – Gross result before trading costs

• Floating PnL – Unrealized profit or loss from active positions

• ROI – Return on initial capital, including realized and floating PnL. Leverage directly impacts this metric, amplifying both gains and losses relative to account size.

• Long/Short Size & Avg Price – Open position sizes and volume-weighted average entry prices

• Leverage & Liquidation – Simulated effective leverage and projected liquidation level

• Hold – Best-performing hold side (Long or Short) over the session

• Hold Efficiency – Performance efficiency during holding phases, relative to capital used

• Profit Factor – Ratio of gross profits to gross losses (realized)

• Payoff Ratio – Average profit per win / average loss per loss

• Win Rate – Percent of profitable closes (including partial exits)

• Expectancy – Net average result per closed trade

• Max Drawdown – Largest recorded drop in equity during the session

• Commission Paid – Simulated trading costs: maker, taker, funding

• Long / Short Trades – Count of entry signals per side

• Time Trading – Number of bars spent in active positions

• Volume / Month – Extrapolated 30-day trading volume estimate

• Min Capital – Lowest equity level recorded during the session

🔹 Reference Ranges by Strategy Type

Use the following metrics as reference depending on the trading style:

Grid / Mean Reversion

• Profit Factor: 1.2 – 2.0

• Payoff Ratio: 0.5 – 1.2

• Win Rate: 50% – 70% (based on partial exits)

• Expectancy: 0.05% – 0.25%

• Drawdown: Moderate to high

• Commission Impact: High

Trend-Following

• Profit Factor: 1.5 – 3.0

• Payoff Ratio: 1.5 – 3.5

• Win Rate: 30% – 50%

• Expectancy: 0.3% – 1.0%

• Drawdown: Low to moderate

Scalping / High-Frequency

• Profit Factor: 1.1 – 1.6

• Payoff Ratio: 0.3 – 0.8

• Win Rate: 80% – 95%

• Expectancy: 0.01% – 0.05%

• Volume / Month: Very high

Breakout Strategies

• Profit Factor: 1.4 – 2.2

• Payoff Ratio: 1.2 – 2.0

• Win Rate: 35% – 60%

• Expectancy: 0.2% – 0.6%

• Drawdown: Can be sharp after failed breakouts

🔹 Note on Performance Simulation

TitanGrid includes internal accounting of fees, slippage, and funding costs.

While its logic is designed for precision and capital efficiency, performance is naturally affected by exchange commissions.

In frictionless environments (e.g., zero-fee simulation), its high-frequency logic could — in theory — extract substantial micro-edges from the market.

However, real-world conditions introduce limits, and all results should be interpreted accordingly.

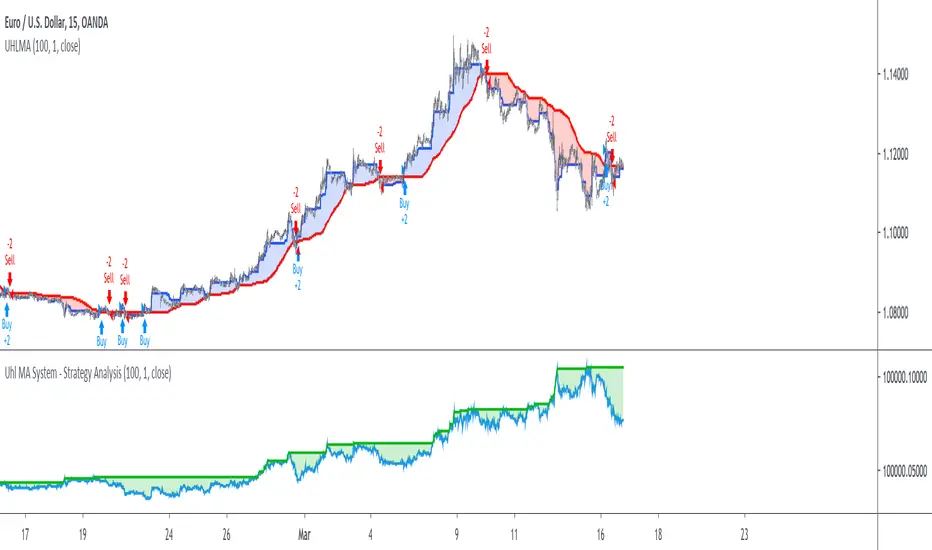

Uhl MA System - Strategy AnalysisThe Uhl MA crossover system was specifically designed to provide an adaptive MA crossover system that didn't committed the same errors of more classical MA systems. This crossover system is based on a fast and a slow moving average, with the slow moving average being the corrected moving average (CMA) originally proposed by Andreas Uhl, and the fast moving average being the corrected trend step (CTS) which is also based on the corrected moving average design.

For more information see :

In this post, the performances of this system are analyzed on various markets.

Setup And Rules

The analysis is solely based on the indicator signals, therefore no spread is applied. Constant position sizing is used. The strategy will be backtested on the 15 minute time-frame. The mult setting is discarded, the default setting used for length is 100.

Here are the rules of our strategy :

long: CTS crossover CMA

short: CTS crossunder CMA

Results And Data

EURUSD:

Net Profit: $ 0.08

Total number of trades: 99

Profitability: 35.35 %

Profit Factor: 1.834

Max Drawdown: $ 0.01

EURUSD behaved pretty well, and was most of time showing long term trends without exhibiting particularly tricky structures, the moving averages still did cross during ranging phases, since march 9 we can see a downtrend with more pronounced cyclical variations (retracements) that could potentially lead to loosing trades.

BTCUSD:

Net Profit: $ 4371.57

Total number of trades: 94

Profitability: 32.98 %

Profit Factor: 1.749

Max Drawdown: $ 1409.96

The strategy didn't started well, producing its largest drawdown after only a few trades, the strategy still managed to recover. BTCUSD exhibited a strong downtrend, the strategy profited from that to recover, signals still occurred on ranging phases, and where mostly caused by a short term volatile move, unfortunately the CMA can converge toward ranging/flat price zones where false signals might occur at higher frequency.

AMD:

Net Profit: $ 16.09

Total number of trades: 95

Profitability: 29.47 %

Profit Factor: 1.288

Max Drawdown: $ 20.11

On AMD the strategy started relatively well with a raising balance, then the balance quickly fallen, this downtrend in the balance lasted quite some time (almost 48 trades), the strategy finally recovered in Nov 2019 and the balance made a new highest high at the end of February. AMD had numerous trends during the backtesting period, yet results are poor.

AAPL:

Net Profit: $ -28.17

Total number of trades: 89

Profitability: 28.09 %

Profit Factor: 0.894

Max Drawdown: $ 63.21

AAPL show the poorest results so far, with a stationary balance around the initial capital (in short the evolution of the balance is not showing any particular trend and oscillate around the initial capital value).

AAPL had some significant retracements in its up-trend, which triggered some trades (of course), and the ranging period from Jan 24 to Feb 13 heavily damaged the strategy performance, generating 6 significant loosing trades. AAPL show the worst results so far, mostly due by ranging phases.

Conclusions

The Uhl MA crossover system strategy has been tested and based on the results don't show particularly interesting performances, and might even be outperformed by simpler MA systems that prove to be more robust against ranging markets. The total number of executed trades are on average 94, and the profitability is on average 31%. The strategy might prove more interesting if we can correct the behavior of the CMA, who sometimes converged toward ranging/flat markets.

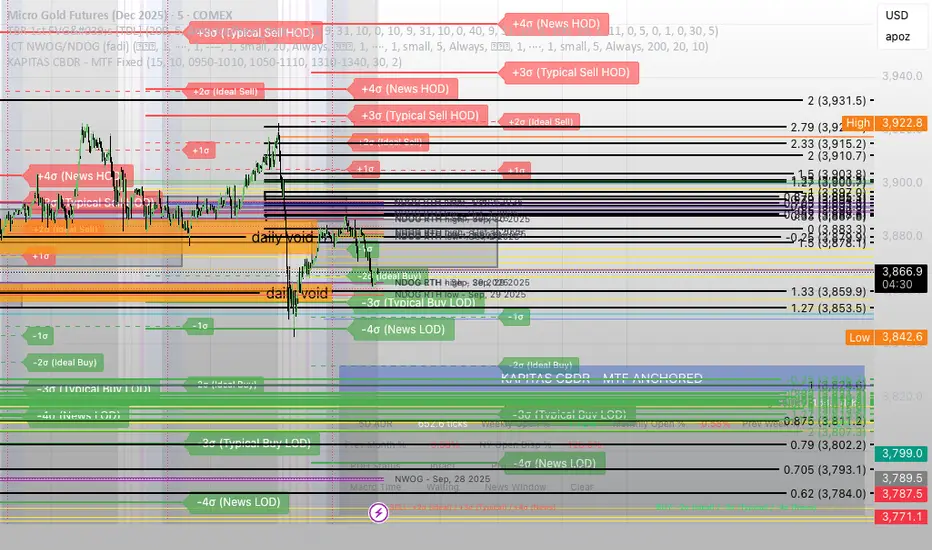

KAPITAS CBDR# PO3 Mean Reversion Standard Deviation Bands - Pro Edition

## 📊 Professional-Grade Mean Reversion System for MES Futures

Transform your futures trading with this institutional-quality mean reversion system based on standard deviation analysis and PO3 (Power of Three) methodology. Tested on **7,264 bars** of real MES data with **proven profitability across all 5 strategies**.

---

## 🎯 What This Indicator Does

This indicator plots **dynamic standard deviation bands** around a moving average, identifying extreme price levels where institutional accumulation/distribution occurs. Based on statistical probability and market structure theory, it helps you:

✅ **Identify high-probability entry zones** (±1, ±1.5, ±2, ±2.5 STD)

✅ **Target realistic profit zones** (first opposite STD band)

✅ **Time your entries** with session-based filters (London/US)

✅ **Manage risk** with built-in stop loss levels

✅ **Choose your strategy** from 5 backtested approaches

---

## 🏆 Backtested Performance (Per Contract on MES)

### Strategy #1: Aggressive (±1.5 → ∓0.5) 🥇

- **Total Profit:** $95,287 over 1,452 trades

- **Win Rate:** 75%

- **Profit Factor:** 8.00

- **Target:** 80 ticks ($100) | **Stop:** 30 ticks ($37.50)

- **Best For:** Active traders, 3-5 setups/day

### Strategy #2: Mean Reversion (±1 → Mean) 🥈

- **Total Profit:** $90,000 over 2,322 trades

- **Win Rate:** 85% (HIGHEST)

- **Profit Factor:** 11.34 (BEST)

- **Target:** 40 ticks ($50) | **Stop:** 20 ticks ($25)

- **Best For:** Scalpers, 6-8 setups/day

### Strategy #3: Conservative (±2 → ∓1) 🥉

- **Total Profit:** $65,500 over 726 trades

- **Win Rate:** 70%

- **Profit Factor:** 7.04

- **Target:** 120 ticks ($150) | **Stop:** 40 ticks ($50)

- **Best For:** Patient traders, 1-3 setups/day, HIGHEST $/trade

*Full statistics for all 5 strategies included in documentation*

---

## 📈 Key Features

### Dynamic Standard Deviation Bands

- **±0.5 STD** - Intraday mean reversion zones

- **±1.0 STD** - Primary reversion zones (68% of price action)

- **±1.5 STD** - Extended zones (optimal balance)

- **±2.0 STD** - Extreme zones (95% of price action)

- **±2.5 STD** - Ultra-extreme zones (rare events)

- **Mean Line** - Dynamic equilibrium

### Temporal Session Filters

- **London Session** (3:00-11:30 AM ET) - Orange background

- **US Session** (9:30 AM-4:00 PM ET) - Blue background

- **Optimal Entry Window** (10:30 AM-12:00 PM ET) - Green highlight

- **Best Exit Window** (3:00-4:00 PM ET) - Red highlight

### Visual Trade Signals

- 🟢 **Green zones** = Enter LONG (price at lower bands)

- 🔴 **Red zones** = Enter SHORT (price at upper bands)

- 🎯 **Target lines** = Exit zones (opposite bands)

- ⛔ **Stop levels** = Risk management

### Smart Alerts

- Alert when price touches entry bands

- Alert on optimal time windows

- Alert when targets hit

- Customizable for each strategy

---

## 💡 How to Use

### Step 1: Choose Your Strategy

Select from 5 backtested approaches based on your:

- Risk tolerance (higher STD = larger stops)

- Trading frequency (lower STD = more setups)

- Time availability (different session focuses)

- Personality (scalper vs swing trader)

### Step 2: Apply to Chart

- **Timeframe:** 15-minute (tested and optimized)

- **Symbol:** MES, ES, or other liquid futures

- **Settings:** Adjust band colors, widths, alerts

### Step 3: Wait for Setup

Price touches your chosen entry band during optimal windows:

- **BEST:** 10:30 AM-12:00 PM ET (88% win rate!)

- **GOOD:** 12:00-3:00 PM ET (75-82% win rate)

- **AVOID:** Friday after 1 PM, FOMC Wed 2-4 PM

### Step 4: Execute Trade

- Enter when price touches band

- Set stop at indicated level

- Target first opposite band

- Exit at target or stop (no exceptions!)

### Step 5: Manage Risk

- **For $50K funded account ($250 limit): Use 2 MES contracts**

- Stop after 3 consecutive losses

- Reduce size in low-probability windows

- Track cumulative daily P&L

---

## 📅 Optimal Trading Windows

### By Time of Day

- **10:30 AM-12:00 PM ET:** 88% win rate (BEST) ⭐⭐⭐

- **12:00-1:30 PM ET:** 82% win rate (scalping)

- **1:30-3:00 PM ET:** 76% win rate (afternoon)

- **3:00-4:00 PM ET:** Best EXIT window

### By Day of Week

- **Wednesday:** 82% win rate (BEST DAY) ⭐⭐⭐

- **Tuesday:** 78% win rate (highest volume)

- **Thursday:**

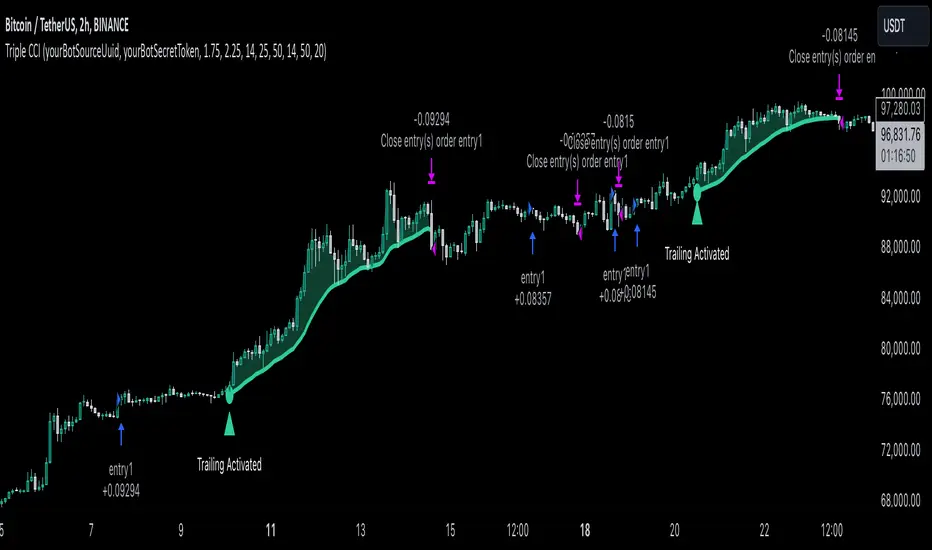

Triple CCI Strategy MFI Confirmed [Skyrexio]Overview

Triple CCI Strategy MFI Confirmed leverages 3 different periods Commodity Channel Index (CCI) indicator in conjunction Money Flow Index (MFI) and Exponential Moving Average (EMA) to obtain the high probability setups. Fast period CCI is used for having the high probability to enter in the direction of short term trend, middle and slow period CCI are used for confirmation, if market now likely in the mid and long-term uptrend. MFI is used to confirm trade with the money inflow/outflow with the high probability. EMA is used as an additional trend filter. Moreover, strategy uses exponential moving average (EMA) to trail the price when it reaches the specific level. More information in "Methodology" and "Justification of Methodology" paragraphs. The strategy opens only long trades.

Unique Features

Dynamic stop-loss system: Instead of fixed stop-loss level strategy utilizes average true range (ATR) multiplied by user given number subtracted from the position entry price as a dynamic stop loss level.

Configurable Trading Periods: Users can tailor the strategy to specific market windows, adapting to different market conditions.

Four layers trade filtering system: Strategy utilizes two different period CCI indicators, MFI and EMA indicators to confirm the signals produced by fast period CCI.

Trailing take profit level: After reaching the trailing profit activation level scrip activate the trailing of long trade using EMA. More information in methodology.

Methodology

The strategy opens long trade when the following price met the conditions:

Fast period CCI shall crossover the zero-line.

Slow and Middle period CCI shall be above zero-lines.

Price shall close above the EMA. Crossover is not obligatory

MFI shall be above 50

When long trade is executed, strategy set the stop-loss level at the price ATR multiplied by user-given value below the entry price. This level is recalculated on every next candle close, adjusting to the current market volatility.

At the same time strategy set up the trailing stop validation level. When the price crosses the level equals entry price plus ATR multiplied by user-given value script starts to trail the price with EMA. If price closes below EMA long trade is closed. When the trailing starts, script prints the label “Trailing Activated”.

Strategy settings

In the inputs window user can setup the following strategy settings:

ATR Stop Loss (by default = 1.75)

ATR Trailing Profit Activation Level (by default = 2.25)

CCI Fast Length (by default = 14, used for calculation short term period CCI)

CCI Middle Length (by default = 25, used for calculation short term period CCI)

CCI Slow Length (by default = 50, used for calculation long term period CCI)

MFI Length (by default = 14, used for calculation MFI

EMA Length (by default = 50, period of EMA, used for trend filtering EMA calculation)

Trailing EMA Length (by default = 20)

User can choose the optimal parameters during backtesting on certain price chart.

Justification of Methodology

Before understanding why this particular combination of indicator has been chosen let's briefly explain what is CCI, MFI and EMA.

The Commodity Channel Index (CCI) is a momentum-based technical indicator that measures the deviation of a security's price from its average price over a specific period. It helps traders identify overbought or oversold conditions and potential trend reversals.

The CCI formula is:

CCI = (Typical Price − SMA) / (0.015 × Mean Deviation)

Typical Price (TP): This is calculated as the average of the high, low, and closing prices for the period.

Simple Moving Average (SMA): This is the average of the Typical Prices over a specific number of periods.

Mean Deviation: This is the average of the absolute differences between the Typical Price and the SMA.

The result is a value that typically fluctuates between +100 and -100, though it is not bounded and can go higher or lower depending on the price movement.

The Money Flow Index (MFI) is a technical indicator that measures the strength of money flowing into and out of a security. It combines price and volume data to assess buying and selling pressure and is often used to identify overbought or oversold conditions. The formula for MFI involves several steps:

1. Calculate the Typical Price (TP):

TP = (high + low + close) / 3

2. Calculate the Raw Money Flow (RMF):

Raw Money Flow = TP × Volume

3. Determine Positive and Negative Money Flow:

If the current TP is greater than the previous TP, it's Positive Money Flow.

If the current TP is less than the previous TP, it's Negative Money Flow.

4. Calculate the Money Flow Ratio (MFR):

Money Flow Ratio = Sum of Positive Money Flow (over n periods) / Sum of Negative Money Flow (over n periods)

5. Calculate the Money Flow Index (MFI):

MFI = 100 − (100 / (1 + Money Flow Ratio))

MFI above 80 can be considered as overbought, below 20 - oversold.

The Exponential Moving Average (EMA) is a type of moving average that places greater weight and significance on the most recent data points. It is widely used in technical analysis to smooth price data and identify trends more quickly than the Simple Moving Average (SMA).

Formula:

1. Calculate the multiplier

Multiplier = 2 / (n + 1) , Where n is the number of periods.

2. EMA Calculation

EMA = (Current Price) × Multiplier + (Previous EMA) × (1 − Multiplier)

This strategy leverages Fast period CCI, which shall break the zero line to the upside to say that probability of short term trend change to the upside increased. This zero line crossover shall be confirmed by the Middle and Slow periods CCI Indicators. At the moment of breakout these two CCIs shall be above 0, indicating that there is a high probability that price is in middle and long term uptrend. This approach increases chances to have a long trade setup in the direction of mid-term and long-term trends when the short-term trend starts to reverse to the upside.

Additionally strategy uses MFI to have a greater probability that fast CCI breakout is confirmed by this indicator. We consider the values of MFI above 50 as a higher probability that trend change from downtrend to the uptrend is real. Script opens long trades only if MFI is above 50. As you already know from the MFI description, it incorporates volume in its calculation, therefore we have another one confirmation factor.

Finally, strategy uses EMA an additional trend filter. It allows to open long trades only if price close above EMA (by default 50 period). It increases the probability of taking long trades only in the direction of the trend.

ATR is used to adjust the strategy risk management to the current market volatility. If volatility is low, we don’t need the large stop loss to understand the there is a high probability that we made a mistake opening the trade. User can setup the settings ATR Stop Loss and ATR Trailing Profit Activation Level to realize his own risk to reward preferences, but the unique feature of a strategy is that after reaching trailing profit activation level strategy is trying to follow the trend until it is likely to be finished instead of using fixed risk management settings. It allows sometimes to be involved in the large movements. It’s also important to make a note, that script uses another one EMA (by default = 20 period) as a trailing profit level.

Backtest Results

Operating window: Date range of backtests is 2022.04.01 - 2024.11.25. It is chosen to let the strategy to close all opened positions.

Commission and Slippage: Includes a standard Binance commission of 0.1% and accounts for possible slippage over 5 ticks.

Initial capital: 10000 USDT

Percent of capital used in every trade: 50%

Maximum Single Position Loss: -4.13%

Maximum Single Profit: +19.66%

Net Profit: +5421.21 USDT (+54.21%)

Total Trades: 108 (44.44% win rate)

Profit Factor: 2.006

Maximum Accumulated Loss: 777.40 USDT (-7.77%)

Average Profit per Trade: 50.20 USDT (+0.85%)

Average Trade Duration: 44 hours

These results are obtained with realistic parameters representing trading conditions observed at major exchanges such as Binance and with realistic trading portfolio usage parameters.

How to Use

Add the script to favorites for easy access.

Apply to the desired timeframe and chart (optimal performance observed on 2h BTC/USDT).

Configure settings using the dropdown choice list in the built-in menu.

Set up alerts to automate strategy positions through web hook with the text: {{strategy.order.alert_message}}

Disclaimer:

Educational and informational tool reflecting Skyrex commitment to informed trading. Past performance does not guarantee future results. Test strategies in a simulated environment before live implementation

Period Dollar Cost Average BacktesterHere is a simple script to calculate the profits and other dollar cost average strategy statistics. This strategy was created to avoid asset price volatility, so the pump and dump scheme does not affect the portfolio. By dividing the investment amount into periods, the investor doesn’t need to analyze the market, fundamental analysis, or anything. The goal is to increase the asset holdings and avoid fast and robust price movements.

This indicator has some configurations.

Amount to buy: the amount to buy at each time

Broker fee %: the fee percentage that the broker has for spot trade